Today we are talking esports, Amazon and fintech but first...

Seedtable #118 | April 8th

Hey everyone,

This is a fun one.

The complexity in building highly regulated financial products has always been the greatest constraint on financial innovation.

But in the past few years, a growing set of companies (like Stripe) have been designing the Lego blocks to enable others to launch new financial services in a fast, flexible & compliant way.

Let's dive in.

Embedded Fintech

Embedded fintech companies provide services or tech that can be integrated into other companies with a traditionally non-financial product or technology.

Think of credit cards.

When you sign up for a bank you're offered the chance to get a credit card along with your debit card. These credit cards have your bank's name on them, but they're the result of a partnership between your bank and a credit card company, such as Amex or Visa.

In other words: your bank embeds third-party financial technology to provide you with an additional service you can sign up for with no effort.

But now things are changing.

Over the past few years, we've seen not only banks but giants like Apple, Paypal and Amazon offer their customers credit and debit cards to ease their customer experience (and create a new revenue stream at the same time.) That's one example of the modern iteration of embedded finance. But that's just the peak of the iceberg.

There’s also the rise of ‘buy-now-pay-later’ companies, best exemplified by the case of Klarna — one of Europe’s biggest unicorns at a $31 billion valuation. Klarna, in fact, already operates in more than 17 countries, with over 250,000 retail partners including giants such as Macys, H&M, Samsung and Ikea.

And there’s also the advent of embedded insurance, as seen in the case of brussels-based Qover, which recently partnered with (i. e. embedded its tech into) Revolut to provide the neobank’s customers with customized insurance policies.

Now, let’s take a deeper look.

Embedded Fintech is (or soon will be) Everywhere

If you don't believe me, just look at this graph:

|

(Source)

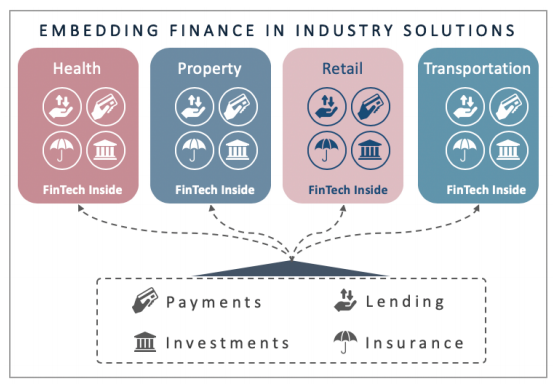

Embedded Fintech can take many forms because, by definition, it works for almost all industries.

Successful companies usually come with embedded, loyal customers that purchase (or subscribe to) their products without thinking twice. The problem is that taking full advantage of those customers' attention and maximizing collected revenue per customer is often hard, and requires startups to set up multiple selling channels.

There's ridesharing, for example. Companies like Uber or Cabify already offer their users various financial products, such as instant payouts and digital wallets. Larger consumer tech companies, such as Apple and Amazon, as we mentioned before, do the same thing; they offer lending, digital wallets, gift cards, P2P payment services — all those are embedded fintech territory.

They can outsource financial services, which makes everything cheaper and faster because the embedded fintech companies are the ones dealing with the technology, ever-changing regulation and bureaucracy involved in the fintech business.

Next, we'll look at some of the different types of embedded fintech companies, with (European) examples for each.

1) Banking as a Service (or BaaS)

Banking as a Service companies provide other companies with banking services without having to apply for their own banking license, through simple APIs that are easy and fast to integrate.

- Railsbank (€46.6m)

- Solaris Bank (€155.1M)

- Crassula (unreported) (banking for Paysend)

- Banxware (€4m)

- Starling Bank (€774m) (banking for Square)

- ClearBank (€72m) (banking for Oaknorth)

2) Embedded Payments

These are probably the most popular iteration of embedded fintech right now. Embedded payments companies remove the friction and complexity of creating payment processing technology for their customers to use when they buy (or subscribe to) their products online.

- Shieldpay (€10.9m)

- Satispay (€155m)

- GoCardless (€198m) (payments for Tripadvisor)

- Primer (€22.1m)

- Checkout.com (€755m) (payments for Deliveroo)

- Klarna (€2.5b) (buy-now-pay-later for Gymshark)

- Currencycloud (€171m)

- Scalapay (n/a) (buy-now-pay-later for Decathlon)

- Trustly (€23m)

- Paybase (€8.9m)

- Rapyd (€427m) (payments for Ikea)

3) Embedded Lending & Financing

This is a new(ish) form of embedded fintech, with which companies can integrate services that allow them to lend money or finance purchases to their users, at little to no additional cost. Use cases go from home purchase or rental deposit financing to enabling payment plans or installments and buy-now-pay-later purchases.

- Fellow Pay (€740k)

- Flatfair (n/a) (lending for Vaboo)

- October (€55m)

- Divido (€16.1m) (lending for Lenovo)

- Worig (€63.6k)

4) Embedded Insurance

This is an interesting one, for it allows companies to give their users the option to purchase insurance (pet, health, fire, car rental, you name it) without leaving their platform.

- wefox (€241m)

- Bsurance (€4.5m) (insurance for playbrush)

- Zego (€183m) (insurance for Deliveroo)

- Qover (€15m) (insurance for Revolut)

5) Open Banking and Infrastructure

These are the companies working on the layers beneath all the embedded fintech mentioned above; the ones creating the tech infrastructure that enable all those companies.

- FintechOS (€14.4m)

- Thought Machine (€139m) (Cloud banking for Curve)

- Mambu (€153m) (Cloud banking for N26)

- Tink (€285m) (infrastructure solutions for Paypal)

- OpenFin (€42.8m) (infrastructure solutions for Barclays)

- TrueLayer (€42.8m) (infrastructure solutions for Revolut)

- Ledger (€86.7m)

Why you should care about embedded fintech (now)

As I mentioned above, Embedded Fintech is great because it 1) simplifies companies lives when trying to implement new technologies; 2) enables them to create new revenue and profit streams and, in doing so, 3) allows them to significantly improve user/customer experience (and loyalty).

And it gets better — fintechs (those who focus on the end-user) can leverage their existing technology and offer it as an embedded software/service to other non-fintech companies, which means they too get to create new revenue and profit streams for their business.

This is speeding up two trends:

- Non-fintech companies can now launch financial services using existing distribution. Think Revolut launching insurance within their app.

- New fintech startups can now build innovative products without having to build the plumbing themselves. Think all the fintech companies runningthat run on top of Stripe.

Trends: Why now?

There are three major trends that enable the rise of embedded fintech. These are:

#1 — Consumer Buying Behaviors: More and more (and in large part due to Covid) consumers are doing everything online. This means that the space for embedded fintech to handle most if not all financial services for non-financially-focused companies seeking to meet that digital consumer requirement is widening.

#2 — Sharing of personal data: This may come to an end soon, but as of now, consumers are willing (they don't even care, to be honest) to share their personal data with the companies they interact with. This means that using that data, non-fintech companies can leverage embedded fintech services to provide personalized buying experiences for their users/customers.

The third trend is that of open, transparent, and friendly cooperation between embedded fintech players, and governments. This is best illustrated through a look at EU (and UK, now that Brexit is a thing) regulation.

EU Regulation

In recent years, there have been two notable European initiatives that facilitated the initial rise and growth of embedded fintech. These were:

The EU Passporting System basically means that all banks and e-money institutions in the European Economic Area that get licensed to operate in one country can also operate in any other European country (hence the name 'passporting'). This, evidently, has skyrocketed embedded fintech companies' ability to scale.

The EU Payment Service Directive (PSD2)

This directive, aimed at creating safer and more innovative payment services has become the main facilitator of all payment-related embedded fintech — by enabling a customer agency model where data is sourceds or payments are made by an institution on behalf of someone else. It also helped define the regulatory environment around most Open Banking technology by enabling open the development of APIs that can get third-party access to banking data.

Investor Appetite

Embedded fintech has attracted a lot of investor interest (both at the individual and institutional level.) In fact (and globally speaking), the embedded fintech space is projected to be a $7.2 trillion market opportunity by 2030 (just consider the fact the top 30 banks & insurance account for about $3.5 trillion.)

At the time of writing, the latest European embedded fintech to raise a funding round was Berlin-based Banxware — they offer loans for SMEs in partnership with payment providers, marketplaces, and others. The round totaled €4 million in seed money and was led by Force Over Mass and VR ventures. What's even more notable? Banxware was launched in December of last year.

Force Over Mass and VR ventures are not the only investors interested in enabling (and profiting from) the rise of embedded fintech. Here are some of the investors betting on the European Embedded Fintech scene:

Funds

- High-Tech Gründerfonds (invested in Banxware)

- Fidelity (invested in Starling Bank)

- RPMI Railpen (invested in Starling Bank)

- Kima Ventures (invested in Railsbank)

- Clocktower Technology Ventures (invested in Railsbank)

- Middlegame Ventures (invested in Railsbank)

- Creandum (invested in Clearbank, Creandum)

- Goodwater Capital (invested in Clearbank)

- Passion Capital (invested in Clearbank & GoCardless)

- HV Capital (invested in Clearbank)

- Yabeo Capital (invested in Clearbank)

- Force Over Mass Capital (invested in Shieldpay, Banxware)

- Accel (invested in GoCardless, Primer)

- Balderton Capital (invested in GoCardless, Primer, Zego)

- Bain Capital Ventures (invested in GoCardless, OpenFin)

- Seedcamp (invested in Primer, wefox)

- Speedinvest (invested in Primer, wefox)

- Insight Partners (invested in Checkout.com, Tink)

- Blossom Capital (invested in Checkout.com)

- Atomico (invested in Klarna)

- Sequoia Capital (invested in Klarna)

- Partech (invested in October)

- Draper Esprit (invested in Thought Machine, Ledger)

- Connect Ventures (invested in TrueLayer)

- XAnge (invested in Ledger)

Angels

- Harald McPike (invested in Starling Bank)

- Chris Adelsbach (invested in Railsbank)

- Tim Levene (invested in Railsbank)

- Phillip Riese (invested in Railsbank)

- Peter Jackson (invested in Railsbank)

- Cameron Parry (invested in Railsbank)

- Theo Osborne (invested in Shieldpay)

- Chris Adelsbach (invested in Shieldpay)

- Filip Tysander (invested in Klarna)

- Jonas Nordlander (invested in Klarna)

- Filip Engelbert (invested in Klarna)

- Victor Jacobsson (invested in Klarna)

- Niklas Adalberth (invested in Klarna)

- Sebastian Siemiatkowski (invested in Klarna)

- Ashton Kutcher (invested in wefox)

- Julian Teicke (invested in wefox)

- Amir Suissa (invested in wefox)

- Filippo Privitera (invested in TrueLayer)

- Tony Jamous (invested in TrueLayer)

- Eric Nadalin (invested in TrueLayer)

Challenges

Embedded Fintech comes with one major challenge: widespread acceptance.

All things financial require trust (both at the end-user and enterprise level). While a lot of embedded fintech companies are making a name for themselves and growing exponentially, that doesn't necessarily mean all such companies will be trusted to handle sensitive financial information.

Adopting embedded finance opens companies (and users/customers) up to the possibility of fraud. You might say that that isn't the case — that we've been using embedded fintech in things like credit cards, or Stripe, and that everyone basically trusts them to handle their financial information. And that's true. But that might not be the case with deeper, more complex things such as Open Banking and financial infrastructure technology.

Another challenge to the space is that while everyone can offer financial products, not everyone is actually ready to do it, even if they wanted to. Embedded fintech is a very complicated area of tech, and there is a lack of access to specialized knowledge and relationships which prevents new players from entering the industry.

Moreover, the ecosystem as it stands now is fragmented into different groups — there’s no umbrella community tying all the different types of embedded fintech companies. And a fragmented ecosystem is a weak ecosystem.

🐟 More on the future of protein: Lab-grown tuna steaks could reel in our overfishing problem

🚙 Machine learning gets physical, starting with self-driving cars

💰 Europe’s most prominent VCs ranked in new list for 2021

🛒 Introducing the Deliveroo ‘mafia’

🎤 An interesting conversation between Sifted and Index Ventures fintech team

🤔 The future of neobroking is… social networks?

📈 The 18 startups to watch in southeastern Europe, picked by top VCs

🇫🇷 France’s privacy watchdog probes Clubhouse after complaint and petition

🇪🇸 This I’m excited for: Spain will experiment with four-day workweek, a first for Europe ; will it work?

😨 Amazon’s European workers are plotting action on an epic scale

🍖 Israel is a fake meat powerhouse

👩💼 Diversity and European tech; what does the future look like?

👵 AgeTech: How technology could drastically benefit an ageing society

👨💻 How no-code tech is changing companies big and small

🇬🇧 Regulation time: UK’s Digital Markets Unit starts work on pro-competition reforms

🧈 Butter is building an ‘all-in-one’ platform to run virtual workshops, raises $3.2 million

💸 Stock trading app Freetrade raises $69 million

⚰️ After its near-death experience, AR pioneer Blippar is back with $5M in funding and a B2B model

🪑 D2C furniture startup Tylko closes $26M Series C growth round led by Pitango and Evli

👨⚕️ Insuretech startup Counterpart raises $10M in funding round led by Valor Equity Partners

👩💼 Belgium-based employee engagement platform Ambassify raises €2 million

😃 Helsinki-based open source software outfit Aiven scores $100 million round led by Atomico

🦄 Tel-Aviv/Los Angeles-based Orca Security closes $210 million series C round, reaches unicorn status with $1.2 billion valuation

🏟 London-based Hopin puts the new money to work, acquires Streamable and Jamm

🩺 Birmingham/Porto-based medtech Adapttech raises £2 million

🌊 Helsinki-based martech Sellforte raises €4 million

🤖 London-based edge AI firm LGN raises $2 million

👨💼 Paris-based Breega closes third fund at €110 million

💼 Berlin-based business intelligence tool y42 raises $2.9 million

🤓 Utrecht-based “people-centric” ERP firm Unit4 snapped up for $2+ billion

👀 Berlin-based hyperautomation software firm Camunda closes €82 million Series B round

🤑 London fintech Profile Software acquires Stockholm-based Euronext Centevo, gains Nordic market entry

👩🏫 Paris-based edtech Lalilo acquired by US-based Renaissance

🏡 London-based short term rental manager GuestReady acquires The Porto Concierge

💳 London-based fintech Pollinate raises $50 million in Series C round

☝️ Tel-Aviv-based crypto infrastructure provider Fireblocks raises $133 million in Series-C funding